The risk of rate hikes has increased after the U.S.-Iran failed talks. The likelihood comes after months of what many thought to be a soft landing.

But the fresh uncertainty around the Iran war has now sent shockwaves through global markets, with major advanced economies following a cautious approach towards the 2% target inflation rate.

Recent data on Producer Price Index shows weaker-than-estimated Producer Price Index with significant gains in inflation measures closely followed by the Federal Reserve in March. The report shows that nearly half of the March advance in the index for final demand goods was attributable to a 15.7% rise in gasoline prices. The indexes for diesel fuel, jet fuel, home heating oil, meats, and primary basic organic chemicals also increased.

Interest rate cuts ahead of easing inflation

In the past, the Fed has shown that it doesn’t have to wait for the inflation to hit the exact 2% target. That’s because the central bank policy works with long and variable lags and not in real time.

Research from the Dallas Fed shows oil shocks tend to push headline inflation up sharply, while the impact on core PCE inflation is smaller, unless higher energy prices begin to affect broader inflation and expectations.

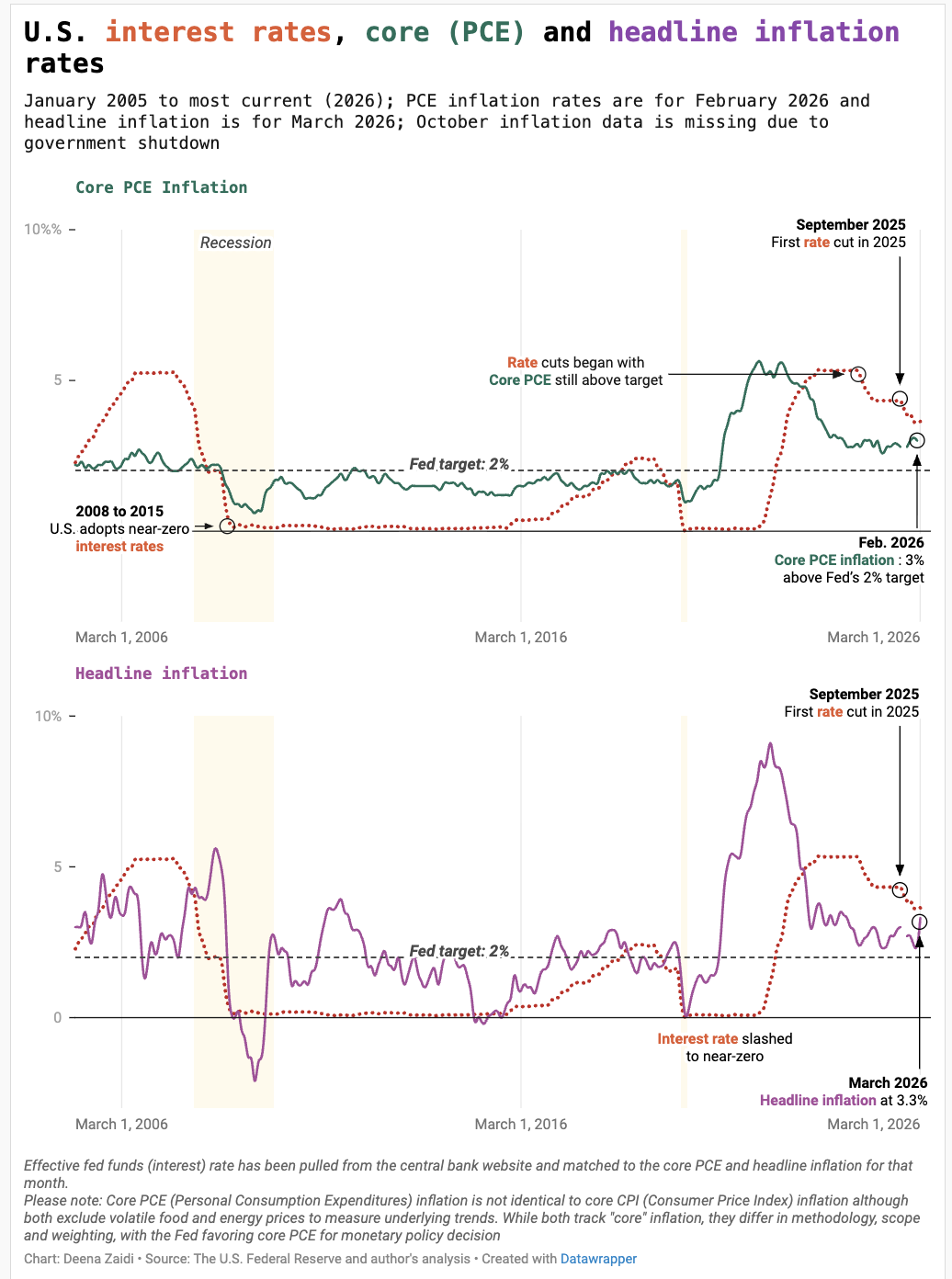

This explains why in September 2025, the Fed began cutting rates even though its core PCE inflation was around 2.8%, well above its 2% target. The decision to cut interest rates was taken because by the time inflation fell to 2%, the economy could already be slowing.

In other words, if the Fed acts preemptively to cut rates to avoid a recession, it surely will act preemptively to raise rates to curb inflation.

Why a 2026 rate hike is back on the table?

With rising uncertainty, most major central banks are pausing any rushed interest rate decisions, not because 2% target inflation has been reached but because the path forward is unclear.

Central banks typically look through energy shocks unless, of course they begin to affect headline inflation. The Fed typically looks at core PCE inflation and employment data, a dual mandate to maintain low and stable inflation and promote maximum employment.

But that doesn’t mean ignoring the headline inflation.

Headline inflation captures the year-over-year change under all different categories and it is easy to gauge where prices went up or what contributed to a change in the headline inflation.

An example is the recent Consumer Price Index data released by the U.S. Bureau of Labor Statistics, which clearly indicates that energy prices rose by 12.5% year-over-year change in March 2026. The spike was exceptionally high over the month with energy index at 10.9%, which is the largest single-month increase in over 20 years. (since the Hurricane Katrina spike in September 2005)

Oil markets are reacting in real time to geopolitical tensions due to supply disruptions at the Strait of Hormuz. Price swings tied to the Iran conflict are feeding volatility across global markets, something central banks are watching more closely than before.

This does not mean rate hikes are imminent but that the Fed has less confidence on inflation reaching its 2% target. If energy-driven price pressures persist and begin to broaden, policymakers may even keep rates higher for longer or in a more extreme scenario, reconsider further tightening through rate hikes.

Bottom line

How the Iran war unfolds depends on many external factors, especially after the failed talks but suffice to say it will be captured in the oil prices, a commodity market closely tied to this war. This also means that we could see an indirect impact on food prices, especially with fertilizer prices rising due to the strait closure.

The lag effect will of course be captured in the next April inflation data that gets released on May 12, 2026.